Given the increasing longevity of Americans and the costs of providing long-term care, anticipation of the costs should be a major element of every family’s financial planning

Assignment: Given the increasing longevity of Americans and the costs of providing long-term care, anticipation

Assignment Description:

Complete ALL of the bullet points below:

- Given the increasing longevity of Americans and the costs of providing long-term care, anticipation of the costs should be a major element of every family’s financial planning. Current information suggests however, that very few families or individuals give this consideration. What factors might impede this advance planning? What measures might be effective in raising awareness among Americans about this important matter?

- Identify the major factors that have resulted in the shift in utilization from inpatient hospitalization to ambulatory care services. What are the implications of this shift for hospitals, consumers, and the health care delivery system as a whole?

- The recipients of mental health services in the US represent only a small percentage of those in need of services. Discuss the factors that impede access to mental illness treatment.

- Include a screenshot of your note taking from your reading this week.

Please submit one APA formatted paper between 1000 – 1500 words, not including the title and reference page. The assignment should have a minimum of two (2) scholarly sources, in addition to the textbook.

M3 Assignment UMBO – 2

M3 Assignment PLG – 4, 8

M3 Assignment CLO – 5, 7

The following specifications are required for this assignment:

- Length: 1000-1500 words

- Structure: Include a title page and reference page in APA style. These do not count towards the minimal word amount for this assignment.

- References: Use the appropriate APA style in-text citations and references for all resources utilized to answer the questions. Include at least two (2) scholarly sources to support your claims.

- Format: Save your assignment as a Microsoft Word document (.doc or .docx).

- File Name: Name your saved file according to your first initial, last name, and the module number (for example, “RHall Module 1.docx”)

Sample Answer

Caring for Patients

The healthcare sector comprises patients from different walks of life. Care providers must understand the nature of different patients ascribed to the healthcare processes. Patients on either hand ought to be prepared in the event of medical emergencies and other medical care practices (Sultz & Young, 2017). This paper will focus on the different issues that might affect access and quality of medical care for patients.

What factors might impede this advance planning? What measures might be effective in raising awareness among Americans about this important matter?

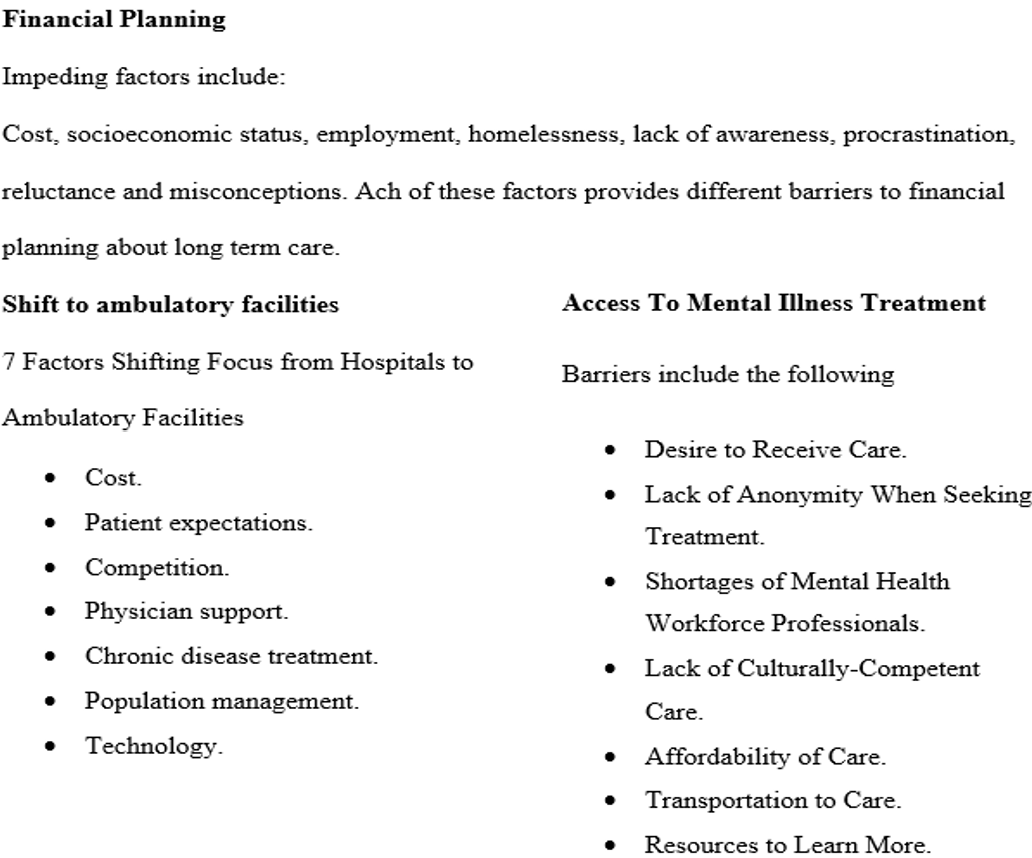

Despite the healthcare sector being an integral part of many families around the world, limited to no financial allocations are put toward safeguarding the future of care. Various factors can impede financial planning associated with the long-term care of families. To begin with, long-term care can be expensive too and those that have insurance covers need to part with a significant amount of money for a specified period (Van Houtven et al., 2020). For many families, affording to set aside finances to cover healthcare needs can be a major challenge.

Low-income families may find it difficult to meet the financial needs of their everyday life and also plan for long-term care. Unemployment is a major issue since it increases overdependence on the family setup. Alternatively, Families may avoid discussing long-term care costs because it can be a sensitive and uncomfortable topic, especially when discussing it with aging parents (Van Houtven et al., 2020). These factors inhibit the ability of the family to afford the financial planning for long-term care.

The other aspect that impedes financial planning for families is a lack of awareness. The majority of the community members are not aware of the high costs of long-term care and may not fully understand the need to plan for it. Individuals tend to downplay the nature and financial obligation of long-term care (Van Houtven et al., 2020). Be that as it may, the majority believe that it would be easy to deal with the other impeding factor is the concern of procrastination.

Individuals may delay planning for long-term care because they assume they will not need it anytime soon, or they are overwhelmed by the complexity of the planning process. There are also misconceptions about insurance coverage which has also surfaced and many people assume that Medicare or health insurance will cover the costs of long-term care, but this is often not the case.

Be that as it may, various ways can be used to create awareness on the issue of financial planning for long-term care. For instance, community education can be a critical process (Fang et al., 2020). Providing educational resources and information about the costs and options for long-term care can help individuals and families better understand the need for planning. Additionally, public campaigns can be a major means to create awareness about the need for financial programming.

Providing educational resources and information about the costs and options for long-term care can help individuals and families better understand the need for planning (Sultz & Young, 2017). Launching public awareness campaigns can help to inform people about the importance of long-term care planning and encourage them to take action (Fang et al., 2020). In this regard, Streamlining and simplifying the process of planning for long-term care costs can make it less overwhelming and more accessible for families.

Identify the major factors that have resulted in the shift in utilization from inpatient hospitalization to ambulatory care services. What are the implications of this shift for hospitals, consumers, and the health care delivery system as a whole?

The shift in utilization from inpatient hospitalization to ambulatory care services has been influenced by several major factors. To begin with, the advances in medical technology and pharmaceuticals have allowed many treatments that previously required hospitalization to be performed on an outpatient basis (DeCook, 2019).

Secondly, there has been a growing emphasis on preventive care, which aims to detect and treat health problems before they require hospitalization. Preventive care helps mitigate the severity of diseases and also detect the disease at an early stage. Third, the rising cost of inpatient hospitalization has led many insurers and consumers to seek more cost-effective alternatives, such as ambulatory care services (Sultz & Young, 2017).

The implications of this shift for hospitals, consumers, and the healthcare delivery system as a whole are significant. For hospitals, the decline in inpatient admissions may result in reduced revenue and a need to restructure their operations to focus more on outpatient care (Carey et al., 2020). Hospitals may also need to invest in new technologies and equipment to provide advanced ambulatory care services.

For consumers, the shift to ambulatory care can result in several benefits, including reduced cost and more convenient access to care. Ambulatory care services are typically less expensive than inpatient hospitalization, and they can be more convenient for patients who do not need the 24-hour monitoring and care provided in a hospital setting (Carey et al., 2020).

Overall, the shift to ambulatory care services represents a significant change in the health care delivery system, with both benefits and challenges for hospitals, consumers, and the system as a whole (Sultz & Young, 2017). As the trend continues, it will be important to monitor its impact on quality, access, and cost of care, and to develop policies and practices that support the continued growth and development of ambulatory care services while ensuring that patients receive safe high-quality care.

The recipients of mental health services in the US represent only a small percentage of those in need of services. Discuss the factors that impede access to mental illness treatment.

Access to mental illness treatment is often impeded by several factors, including stigma, lack of resources, and systemic barriers. The stigma around mental illness can make it difficult for individuals to seek help and can create a barrier to accessing treatment. Many people fear the social and professional consequences of disclosing their mental illness, which can lead to a delay in seeking treatment (McKnight-Eily et al., 2021). Access to mental illness treatment is often impeded by several factors, including stigma, lack of resources, and systemic barriers.

Another factor that can impede access to mental illness treatment is a lack of resources. Mental health services may be unavailable or limited in certain areas, especially in rural or low-income communities (Sultz & Young, 2017). Additionally, there may be long wait times to access mental health care, which can discourage individuals from seeking treatment or exacerbate symptoms while they wait.

Systemic barriers can also make it difficult to access mental illness treatment. Insurance coverage for mental health services may be limited, and individuals may face high out-of-pocket costs for treatment. Furthermore, mental health services may be identified from other aspects of healthcare, making it challenging to coordinate care and access to comprehensive treatment (Taylor & Kuo, 2019).

Access to mental illness treatment is often impeded by several factors, including stigma, lack of resources, and systemic barriers (Sultz & Young, 2017). These barriers can create significant challenges for individuals seeking mental health care and may result in unequal access to services for vulnerable populations. To address these barriers, it is essential to increase public awareness and reduce the stigma surrounding mental illness (Taylor & Kuo, 2019).

Additional resources should be allocated to expanding mental health services in underserved communities, and insurance coverage for mental health services should be improved. Addressing systemic barriers, such as improving coordination of care and reducing discrimination, can also improve access to mental illness treatment.

Conclusion

Caring for patients is an integral part of every nurse and also creates better outcomes. As a result, patients should also be aware of the various factors that would help ensure they receive the best available care. For instance, financial planning and ensuring access to mental health care can help with the processes and increase overall patient outcome. Be that as it may, there is also a need to address barriers to accessing medical care as a means to facilitate all patients to acquire the best care

Screenshot of Notes

References

Carey, K., Morgan, J. R., Lin, M. Y., Kain, M. S., & Creevy, W. R. (2020). Patient outcomes following total joint replacement surgery: a comparison of hospitals and ambulatory surgery centers. The Journal of arthroplasty, 35(1), 7-11.

DeCook, C. A. (2019). Outpatient joint arthroplasty: transitioning to the ambulatory surgery center. The Journal of Arthroplasty, 34(7), S48-S50.

Fang, E. F., Xie, C., Schenkel, J. A., Wu, C., Long, Q., Cui, H., … & Woo, J. (2020). A research agenda for ageing in China in the 21st century: Focusing on basic and translational research, long-term care, policy and social networks. Ageing research reviews, 64, 101174.

McKnight-Eily, L. R., Okoro, C. A., Strine, T. W., Verlenden, J., Hollis, N. D., Njai, R., … & Thomas, C. (2021). Racial and ethnic disparities in the prevalence of stress and worry, mental health conditions, and increased substance use among adults during the COVID-19 pandemic—United States, April and May 2020. Morbidity and Mortality Weekly Report, 70(5), 162.

Sultz, H. A., & Young, K. A. (2017). Health care USA: Understanding its organization and delivery (9th ed.). Jones & Bartlett.

Taylor, R. E., & Kuo, B. C. (2019). Black American psychological help-seeking intention: An integrated literature review with recommendations for clinical practice. Journal of Psychotherapy Integration, 29(4), 325.

Van Houtven, C. H., DePasquale, N., & Coe, N. B. (2020). Essential long‐term care workers commonly hold second jobs and double‐or triple‐duty caregiving roles. Journal of the American Geriatrics Society, 68(8), 1657-1660.

Place your order now for a similar assignment and get fast, cheap and best quality work written by our expert level assignment writers. Limited Offer: NEW30 to Get 30% OFF Your First Order

Limited Offer: NEW30 to Get 30% OFF Your First Order

![]()

Long-Term Care Financial Planning: Essential Strategies for American Families

As American life expectancy continues to rise, the costs of providing long-term care have become a significant financial concern for families nationwide. Given the increasing longevity of Americans and the substantial costs associated with long-term care services, anticipation and planning for these expenses should be a major element of every family’s financial planning strategy.

The Growing Need for Long-Term Care Planning

The demographic shift in America is undeniable. Every day until 2030, 10,000 Baby Boomers will turn 65, creating an unprecedented demand for long-term care services. 70% of seniors will need some type of long-term care, making this a critical planning consideration for virtually every American family.

Current Long-Term Care Statistics (2024-2025)

| Care Type | Annual Cost | Monthly Cost |

|---|---|---|

| Nursing Home (Private Room) | $108,405 | $8,800 |

| Home Health Aide | $61,776 | $5,148 |

| Adult Day Care | $23,400 | $1,950 |

| Assisted Living | $64,200 | $5,350 |

Source: Genworth Cost of Care Survey 2024

Understanding the Financial Impact

Over half (56%) of Americans turning 65 today will develop a disability serious enough to require long-term service and support. More importantly, seniors who require long-term care will need an average of $138,000 worth of long-term support services.

Key Financial Considerations:

- Duration of Care: On average, seniors receive long-term care for three years

- Cost Inflation: Long-term care costs have outpaced inflation for nearly two decades

- Geographic Variations: Costs vary significantly by state and region

Common Barriers to Long-Term Care Planning

Research has identified several significant obstacles that prevent families from adequately planning for long-term care costs:

1. Knowledge Gaps and Denial

- Lack of Awareness: Many Americans underestimate their likelihood of needing long-term care

- Complexity of Options: The array of long-term care options and insurance products can be overwhelming, deterring individuals from engaging in advance planning

- Denial of Aging: Psychological barriers prevent realistic assessment of future needs

2. Financial Constraints

- Competing Priorities: Currently caring for children was a barrier to planning, particularly for making or following through on financial decisions, such as purchasing LTCI or saving for LTC

- High Insurance Costs: Single men paid anywhere from $900 to $1,700, while single women paid from $1,500 to $2,700 for long-term care insurance

- Limited Resources: Many families lack sufficient disposable income for comprehensive planning

3. Systemic Issues

- Inadequate Government Support: Compared with the United States, many other high-income nations have adopted more comprehensive approaches to financing long-term care services

- Insurance Limitations: Medicaid restrictions and Medicare’s limited coverage create gaps

Strategic Financial Planning Solutions

1. Early Planning Benefits

If you wait (say from age 55 to 65) same initial coverage costs 49.9% more. Starting planning early provides:

- Lower insurance premiums

- More time to accumulate savings

- Greater flexibility in care options

2. Diversified Funding Strategies

| Strategy | Pros | Cons | Best For |

|---|---|---|---|

| Long-Term Care Insurance | Dedicated coverage, inflation protection | High premiums, potential for rate increases | Middle to upper-middle income families |

| Self-Insurance/Savings | Flexibility, no premiums | Requires significant assets, market risk | High-net-worth individuals |

| Hybrid Life/LTC Policies | Death benefit if unused, guaranteed premiums | Higher initial cost, complex terms | Those wanting dual protection |

| Health Savings Accounts | Tax advantages, grows over time | Contribution limits, requires HDHP | Working individuals with qualified plans |

3. Comprehensive Planning Framework

Step 1: Assessment

- Calculate potential care costs based on family health history

- Evaluate current financial resources and retirement projections

- Assess risk tolerance and insurance needs

Step 2: Implementation

- Purchase appropriate insurance coverage

- Maximize tax-advantaged savings vehicles

- Create legal documents (powers of attorney, advance directives)

Step 3: Regular Review

- Annual policy reviews and adjustments

- Update planning based on health changes

- Coordinate with overall retirement planning

Overcoming Planning Barriers

Educational Initiatives

- Family Discussions: Making plans for your care later in life is a valuable gift that you can give your family

- Professional Guidance: Consult with financial advisors, elder law attorneys, and insurance specialists

- Resource Utilization: Access online calculators and planning tools

Financial Strategies

- Gradual Implementation: Start with basic coverage and expand over time

- Employer Benefits: Utilize workplace long-term care insurance options

- Government Programs: Understand Medicare and Medicaid eligibility

The Cost of Inaction

Without a unified plan, families might not have enough coverage or savings, leading to out-of-pocket expenses that deplete retirement funds. The financial consequences include:

- Rapid depletion of retirement assets

- Family financial stress and burden

- Limited care options

- Potential family caregiver career disruption

Regional Cost Variations

Long-term care costs vary significantly across the United States, making location-specific planning essential:

Highest Cost States (Annual Nursing Home Costs):

- Alaska: $372,000+

- Connecticut: $150,000+

- Hawaii: $140,000+

- New York: $135,000+

Lowest Cost States:

- Oklahoma: $55,000+

- Louisiana: $60,000+

- Missouri: $65,000+

- Arkansas: $70,000+

Technology and Innovation in Care Planning

Emerging technologies are making long-term care planning more accessible:

- AI-Powered Planning Tools: Automated risk assessment and cost projections

- Telemedicine Integration: Remote monitoring and care coordination

- Digital Health Records: Improved care continuity and family communication

Policy and Legislative Considerations

Recent legislative developments affecting long-term care planning include:

- State-sponsored long-term care programs (Washington State)

- Tax incentives for long-term care insurance

- Medicare Advantage plan expansions

Conclusion

The increasing longevity of Americans, combined with rising long-term care costs, makes financial planning for potential care needs an essential component of comprehensive family financial planning. By understanding the barriers to planning and implementing strategic solutions early, families can protect their financial security while ensuring quality care for their loved ones.

Avoid hard decisions: Decide how you want to be cared for so that your family doesn’t have to decide for you. Protect your assets: Long-term care is expensive and can deplete your retirement assets quickly; have a plan to cover the cost should you need care.

The time to act is now. With proper planning, education, and professional guidance, American families can successfully navigate the complex landscape of long-term care financing and ensure their loved ones receive the care they need without devastating financial consequences.

References and Sources

- American Association for Long-Term Care Insurance. (2024). Long-Term Care Insurance Statistics and Facts. Retrieved from https://www.aaltci.org/long-term-care-insurance/learning-center/ltcfacts-2024.php

- ConsumerAffairs. (2024). Long-Term Care Statistics 2025. Retrieved from https://www.consumeraffairs.com/health/long-term-care-statistics.html

- Genworth Financial. (2024). Cost of Care Survey. Retrieved from https://www.genworth.com/aging-and-you/finances/cost-of-care.html

- National Institute on Aging. (2024). Paying for Long-Term Care. Retrieved from https://www.nia.nih.gov/health/long-term-care/paying-long-term-care

- SingleCare. (2025). Long-term care statistics 2025. Retrieved from https://www.singlecare.com/blog/news/long-term-care-statistics/

- AARP. (2025). Consider Long-Term Care When Planning for the Future. Retrieved from https://www.aarp.org/caregiving/financial-legal/info-2022/planning-for-long-term-care.html

Dan Palmer is a dedicated academic writing specialist with extensive experience supporting nursing students throughout their educational journey. Understanding the unique challenges faced by nursing students who balance demanding clinical rotations, family responsibilities, and rigorous coursework, Dan provides professional assignment assistance that helps students maintain academic excellence without compromising their other commitments.

With a comprehensive understanding of nursing curriculum requirements and academic standards, Dan delivers high-quality, thoroughly researched assignments that serve as valuable learning resources. His expertise spans various nursing disciplines, including clinical practice, healthcare ethics, patient care management, and evidence-based research.

Dan’s approach combines meticulous attention to detail with a commitment to timely delivery, ensuring that busy nursing students receive the support they need when they need it most. His professional assistance has helped countless nursing students successfully navigate their academic programs while maintaining their professional and personal responsibilities.

Committed to academic integrity and excellence, Dan Palmer continues to be a trusted resource for nursing students seeking reliable, professional assignment support.

Related Posts

Examine changes introduced to reform or restructure the U.S. health care delivery system. In a 1,000-1,250 word paper, discuss action taken for reform and restructuring and the role of the nurse within this changing environment.

-

Posted by

Dan Palmer

Dan Palmer

Solved! Address the following topics: Locards principle Basic steps in evidence collection The importance of chain of custody – what is the “locard principle” and how is it important in forensics?

-

Posted by

Dan Palmer

The purpose of this assignment is to synthesize a literature review that will be used to draw conclusions in order to propose an evidence-based practice change to address your identified nurse practice problem

-

Posted by

Dan Palmer

Identify and describe at least two competing needs impacting your selected healthcare issue/stressor

-

Posted by

Dan Palmer

Program policy evaluation is a valuable tool that can help strengthen the quality of programs/policies and improve outcomes for the populations they serve. Program/policy evaluation answers basic questions about program/policy effectiveness.

-

Posted by

Dan Palmer

Describe the setting and access to potential subjects. If there is a need for a consent or approval form, then one must be created. Include a draft of the form as an appendix at the end of your paper

-

Posted by

Dan Palmer

Reflect upon a patient care encounter from personal practice in which multiple “ways of knowing” were used. Illustrate how each fundamental

-

Posted by

Dan Palmer

[Solved] Apply Guidos MORAL model to resolve the dilemma presented in the case study described in Ethical Scenario 4-3 on p. 48 which is titled, “When Care Appears Medically Inappropriate,” (Guido textbook 7th edition)

-

Posted by

Dan Palmer

Managed care organizations emphasize physicians’ responsibilities to control patient access to expensive hospitalization and specialty care, a principle dubbed “gatekeeping.”

-

Posted by

Dan Palmer

[Solved 2025] In this Assignment you will examine the controversy surrounding dissociative disorders. You will also explore clinical, ethical, and legal consideration

-

Posted by

Dan Palmer

[SOLVED 2025] Analyze the similarities and differences between the standards of practice and scope of practice as defined by these entities

-

Posted by

Dan Palmer

Benchmark – Community Teaching Project – Part 2

-

Posted by

Dan Palmer